Portfolio Allocation Entering 2025

I’m a firm believer in portfolio transparency and sharing the positions you own. However, I do understand that some may argue if you share a position you hold, then there’s a bias in your mind that makes it harder for you to admit that you’re wrong, and therefore you may hold a losing position longer than you should.

While that may be true, I do not think that’s the right thing to do if you’re going to share investment ideas. I compare sharing your positions to having an investment advisor that invests their money in the same stocks they have you in or a CEO owning shares in a company you invest in… you want them to invest alongside you and not just give advice they do not follow themselves. If they aren’t doing that, then you should look for a new investment manager or a new company to invest in. They need skin in the game you’re playing, or you probably shouldn’t trust them.

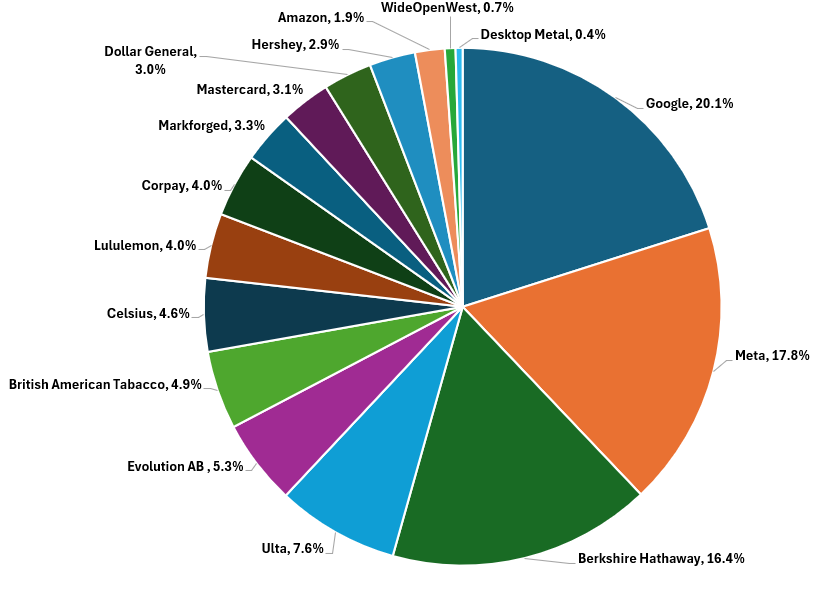

Based on this belief, I have shared my personal portfolio allocation below. I hold 16 positions, with my top 3 holdings making up over 54% of my portfolio (Google, Meta, Berkshire).

When looking at my portfolio, you’ll notice I have extreme concentration in just 3-4 positions. On top of that, majority of my holdings are what I would consider to be long term compounders that I plan to hold for at least 3+ years.

I also own a few special situation investments, which are all mergers (Markforged, Desktop Metals, WideOpenWest). I have smaller allocations here as these may carry more risk if the deals do not go through.

Lastly, as a new contributor to Substack, my plan is to provide an analysis on why I own each investment in my portfolio over the coming months. For the time being I have provided a brief thesis below on my top 5 holdings going into 2025.

Google - This is a compounding machine with a monopoly on search. They have many paths to continue their growth and are one of the cheapest MAG7 companies. When looking at which MAG7 stocks to own you have to ask yourself how do these companies add another $1T+ to their market cap and Google can do this with growth in AI, Cloud, Waymo, and even quantum computing / making chips. This optionality plus trading at a fair PE multiple of 25~ is a great business to continue to hold.

Meta - The easy money has been made on them, but still relatively cheap for their quality. They can continue to add new users and also increase revenues per user. It seems most of the headwinds are behind them from overspending on the Metaverse to Apple making it harder to track user data. Additionally, I think Tiktok while being a competitor has been very beneficial to Meta as governments focus more on the issues of Tiktok instead of seeing Meta as the big scary monster. With the chance of Tiktok also being banned in the US in 2025, this would be a tailwind for Meta that is probably not priced in.

Berkshire Hathaway - Can you really call yourself a value investor if you don’t own Berkshire? While they may now trade much closer to Intrinsic value than previously, I do not have intentions of selling. They have a record cash pile, which owning them is a great hedge as markets are getting frothy again.

ULTA - I do not love owning retail companies as moats in this industry are very difficult. However, ULTA got too cheap in 2024 to overlook. They are still growing topline revenues, and hopefully can maintain 10%+ Net Profit Margins (one of the highest in the retail industry). I believe they are still relatively cheap for their quality, but I will keep a close eye on their margins in 2025. If margins start to decrease more even though Revenues grow, it may make sense to sell now that they have rebounded quite a bit from their lows. If margins stay flat or start to expand again then this could turn out to be a great compounder.

Evolution AB - This is my favorite idea going into 2025. There’s already numerous write ups on Substack about them, and I will put one out in early 2025 as well. Evolution develops, produces, markets and licenses fully integrated B2B Online Casino solutions to gaming operators. Online gaming is a fast growing industry and they have a leading position in this industry. I believe Evolution is setting up similar to Meta in 2022 where all the headwinds are currently hitting them at once (UK investigating them, their labor issues in Georgia, being a sin stock, unregulated markets, etc.), but these issues will eventually turn for the better offering a great entry price today. They currently trade at their lowest valuation ever at a PE and P/FCF of 13~. They also have no debt. Many of the risks seem to be priced in, and I believe a fair PE and PFCF multiple should be 20+, which is already 50% higher than the current multiple and that does not factor in their EPS / FCF growth which should be in the the low teens at least over the next several years. I plan to continue to add at these prices in early 2025.

As always, please let me know your thoughts and share your favorite ideas going into 2025. I hope you have a happy New Year!

-Value Chaser